++++++++++++++++++++

The Largest Car Forum in the Philippines

- Forums

- Discussions

- Events

- Community

Results 2,841 to 2,860 of 10726

-

Tsikot Member Rank 4

Tsikot Member Rank 4

- Join Date

- Nov 2005

- Posts

- 45,927

December 3rd, 2009 05:38 PM #2841Last edited by uls; December 3rd, 2009 at 06:01 PM.

-

Wheelin and Dealin'

Wheelin and Dealin'

- Join Date

- Feb 2008

- Posts

- 14,181

December 3rd, 2009 05:49 PM #2842Another clear example of failure if people try to tinker with the market. In the RP it was prices, in Nokor its the currency...

-

Wheelin and Dealin'

- Join Date

- Feb 2008

- Posts

- 14,181

December 3rd, 2009 06:11 PM #2843Hahaha probably North Koreans are scrambling to spend their old useless money for anything tangible from food, to clothes, to commodities like metal and wood. Hell even plastic crap from China is worth more! The power of paper money, one day its worth this much the next it can be gone. Go for Gold I say!

-

Tsikot Member Rank 4

- Join Date

- Nov 2005

- Posts

- 45,927

December 3rd, 2009 06:37 PM #2844yep

i posted those articles as a reminder of how governments (and their central banks) control people through fiat money manipulationLast edited by uls; December 3rd, 2009 at 06:57 PM.

-

Social Dementia

Social Dementia

- Join Date

- Sep 2003

- Posts

- 25,189

December 3rd, 2009 08:01 PM #2845That is one screwed up country... I hope they'll be screwed enough that the whole goverment collapses like Eastern Europe in the '90s.

-

Tsikot Member Rank 4

- Join Date

- Nov 2005

- Posts

- 45,927

-

Tsikot Member Rank 4

- Join Date

- Nov 2005

- Posts

- 45,927

December 4th, 2009 12:08 PM #2847the other day, Deutsche Bank came out with its 2010 outlook

they present 4 scenarios:

Scenario 1 This scenario is the most optimistic and is one where the authorities have as good a year as they did in 2009. They likely keep stimulus extremely high in the system without there being any noticeable consequences of their actions (e.g. rates at the short and long-end stay low). Under this scenario we would expect equities to be significantly higher, credit spreads be much tighter but with bond yields only edging slightly higher as the authorities are seen to have firm control of inflation expectations and may even be continuing to buy bonds.Scenario 2 This scenario is the most likely and suggests that we start to see gradual easing off the gas from the authorities but only as its proved that there is some momentum in the underlying economy. Under this scenario risk assets have a good year but returns are checked to some degree by rising bond yields and less stimulus being injected into markets. A satisfactory year for risk, especially equities, but a mildly negative one for fixed income. Credit investors will likely have to rely on spreads (and higher beta credit) to get positive total returns.Scenario 3 This is the second most likely scenario overall in 2010 but one that potentially becomes more likely as the year progresses. Here we are likely to see sharply higher bond yields start to disrupt the positive momentum in markets. These higher yields could be either due to Government supply starting to overwhelm demand (especially as the impact of QE, and similar schemes, wane), or because of inflation fears. It seems unlikely that actual inflation will be a concern in 2010 but its quite possible for expectations to become unanchored. We would also have to include the potential for a Sovereign crisis somewhere in the Developed world within this scenario. We would note that the higher yields in this scenario are not based on positive growth momentum but by inflation/Sovereign risk. Such a scenario is incorporated in Scenario 2.according to DB, scenario 1 has a 15% probability of occuringScenario 4 This is the nightmare scenario of Deflation or in less extreme terms perhaps a double-dip. Given that much of the world is currently still in negative YoY inflation territory it is difficult to completely rule out even if we do live in a fiat currency system and even if inflation is expected to return to positive territory in early 2010. For deflation to be sustained we would probably need an exogenous event to hamper the authorities ability to continue to successfully fight this credit crisis. Such events could be a fresh banking crisis arising, a political backlash encouraging immediate increases in 2 December 2009 Macro Credit and Equity Page 4 Deutsche Bank AG/London economic regulation or withdrawal of stimulus, or possibly a Government bond/currency sell-off that forces the authorities to aggressively reign in stimulus for fear of a sovereign crisis. A Sovereign crisis outside the Developed world could also encourage this scenario as there would be a flight to quality into Developed market bond market in spite of the fact that these markets have their own large fiscal issues. Bond yields would eventually rally strongly but risk assets would experience a very poor year. As time progresses this scenario becomes less likely as the system gradually repairs itself and the authorities are allowed more time to inflate the global economy. As we discuss in scenario 3, the more likely risk scenario is inflation, especially as time progresses.

scenario 2 50%,

scenario 3 25%

scenario 4 10%

-

Tsikot Member Rank 4

- Join Date

- Nov 2005

- Posts

- 45,927

-

Tsikot Member Rank 4

- Join Date

- Nov 2005

- Posts

- 45,927

-

Wheelin and Dealin'

- Join Date

- Feb 2008

- Posts

- 14,181

-

Tsikot Member Rank 4

- Join Date

- Nov 2005

- Posts

- 45,927

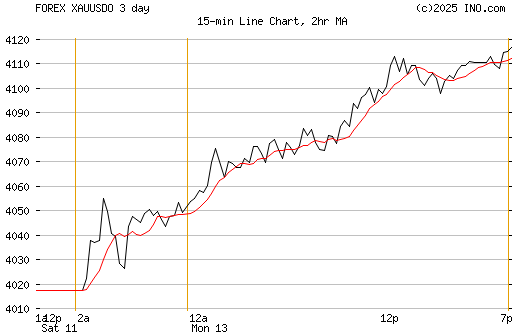

December 5th, 2009 11:11 AM #2851the USD and stocks both skyrocketted at the open

that's unusual coz the USD and stocks have an inverse correlation

they have been moving in opposite direction for more than a year already

USD index

S&P500

at first, i thought the inverse correlation has been broken

nope, it's still there

stocks couldnt go higher with the USD going higher

stocks fell after a sharp rally at the open:

USD index

exciting last trading day for the week

happy weekendLast edited by uls; December 5th, 2009 at 11:19 AM.

-

Wheelin and Dealin'

- Join Date

- Feb 2008

- Posts

- 14,181

-

Tsikot Member Rank 4

- Join Date

- Nov 2005

- Posts

- 45,927

December 5th, 2009 03:16 PM #2853bababa yan

after the jobs data last night, the Fed will be pressured to raise rates sooner rather than later

reversal of the USD carry trade coming soon

-

Tsikot Member Rank 4

- Join Date

- Nov 2005

- Posts

- 45,927

-

Tsikot Member Rank 4

- Join Date

- Nov 2005

- Posts

- 45,927

-

Tsikot Member Rank 4

- Join Date

- Nov 2005

- Posts

- 45,927

December 8th, 2009 11:52 AM #2856Bernanke speech last night

Uncle Ben signals no rate hikes yet

"Though we have begun to see some improvement in economic activity, we still have some way to go before we can be assured that the recovery will be self-sustaining"rates"whether the recovery will be strong enough to create the large number of jobs that will be needed to materially bring down the unemployment rate"

dollar drops"exceptionally low"

"extended period"

gold price rises

Last edited by uls; December 8th, 2009 at 12:00 PM.

-

Tsikot Member Rank 3

Tsikot Member Rank 3

- Join Date

- Sep 2005

- Posts

- 939

-

Social Dementia

- Join Date

- Sep 2003

- Posts

- 25,189

-

Tsikot Member Rank 4

- Join Date

- Nov 2005

- Posts

- 45,927

December 9th, 2009 09:49 AM #2859USD index finds support a bit above 74

52 week low 74.17

--

the Euro's performance is linked to problems with Greece

Greece is toast

the EMU will have to bail out Greece sometime next year

if the EMU lets Greece default, then the Euro is toastLast edited by uls; December 9th, 2009 at 09:53 AM.

-

Tsikot Member Rank 4

- Join Date

- Nov 2005

- Posts

- 45,927

December 9th, 2009 10:11 AM #2860what do you mean po? Originally Posted by froshie1

Originally Posted by froshie1

if diversifying away from the USD, foreign central banks are buying gold

Reply With Quote

Reply With Quote